Case Study • Financial Services • IV&V / Quality Assurance

Hidden Risk: How a Financial Institution Used IV&V to Protect a Critical Banking Application

A Community Bank Offering Commercial, Personal, and Wealth Management Services • Independent Verification and Validation •

IV&V consulting services

The Enterprise Challenge

IV&V Consulting Services for a Mission-Critical Financial Application

A bank committed to helping customers grow personal wealth, finance real estate investments, and manage business banking engaged a third-party vendor to develop a Paying Agency Application – a system that would handle payment processing functions critical to the bank’s operations and its customers’ financial transactions. The bank had defined its requirements, selected the development vendor, and was watching the application take shape. What it needed was an objective answer to a question the development team could not answer about its own work: was the application actually being built correctly?

In financial services, the consequences of a security vulnerability, a compliance gap, or a logic error in a payment application are not abstract. They are regulatory findings, customer data exposure events, and operational failures that affect real accounts and real transactions. The development vendor’s quality assurance process was inherently limited by the team’s familiarity with its own code – the same cognitive investment that makes developers efficient at building also makes them poor at seeing the vulnerabilities in what they have built.

The bank engaged i3solutions to provide IV&V consulting services: an independent assessment of the Paying Agency Application that would objectively verify whether the application met the bank’s requirements, identify and help remediate vulnerabilities before they reached production, ensure compliance with the standards applicable to a financial institution’s payment processing systems, and provide the quality validation that the bank’s stakeholders and regulators expected.

Strategic Trigger

Third-Party Development Created an Objectivity Gap the Bank Had to Fill

The decision to engage IV&V was driven by the recognition that the bank was in a structurally vulnerable position. A third-party vendor was building a critical application. The vendor’s financial interest was in delivering the project and moving to the next engagement – not in surfacing problems that would extend the project timeline. The bank’s own technical team was not resourced to perform a comprehensive independent code review while also managing the vendor relationship and overseeing the project timeline. The objectivity gap was not a reflection on the vendor’s integrity – it was structural, built into the nature of any development relationship where the builder and the validator are the same party.

The payment application’s function intensified the stakes. A Paying Agency Application sits at the intersection of financial transactions, customer data, and regulatory compliance. A security vulnerability in this system was not a theoretical risk to be addressed in the next release cycle. It was a potential exposure of customer financial information and a potential pathway to payment processing fraud that the bank had both regulatory and fiduciary obligations to prevent.

The bank’s commitment to innovative banking products and superior customer service – built on the expectation that technology would enhance rather than undermine customer confidence – made the IV&V investment a straightforward decision. The cost of a thorough independent review was measured against the cost of discovering the same issues after go-live, where industry research consistently shows defects cost an order of magnitude more to fix and significantly more in customer confidence to repair.

Is a critical financial application being built by a third party without independent validation?

If a development vendor is producing a system that handles payment processing, customer financial data, or regulated functions, the objectivity gap is structural. An IV&V engagement identifies what the development team cannot see in its own work before those issues reach production. The 15-Business-Day Microsoft Assessment maps the scope and approach for your specific application.

Request the Assessment

▶ Related Insight — A 60-second perspective from our channel

Stakes (What Happens If They Fail)

Payment Application Vulnerabilities, Regulatory Exposure, and Customer Trust at Risk

For a community bank whose competitive position depends on its reputation for superior customer service and trustworthy financial management, a security breach in a payment application is not a technology incident that can be quietly remediated. It is a customer relationship event that requires regulatory notification, public disclosure, and a sustained effort to restore confidence that takes years to rebuild. The reputational cost of a breach in a financial services institution consistently exceeds the direct financial cost by a multiple that makes prevention investments look inexpensive in retrospect.

The regulatory dimension carried its own specific exposure. Financial institution payment systems are subject to oversight that includes examination of both the security controls in production systems and the development practices that produced them. A system deployed with known vulnerabilities that were not identified because the bank had not performed an independent review is a different regulatory finding from a system where vulnerabilities were identified through IV&V and remediated before deployment. The first suggests inadequate oversight; the second demonstrates a mature risk management approach to technology development.

The operational cost of post-deployment issue discovery was the third dimension of the stakes. Defects found during IV&V – while the development vendor is still engaged and the codebase is still active – cost a fraction of what the same defects cost when they surface in a production system after the vendor relationship has ended and the bank must either re-engage the vendor at change-order rates or find a new partner to diagnose and fix code they did not write.

Constraints and Complexity

Active Development Timeline, Vendor Relationship Management, and Financial Compliance Standards

The IV&V engagement had to operate in parallel with the development vendor’s active project timeline without disrupting the development process or creating a adversarial dynamic in the vendor relationship. The bank needed an IV&V partner who could engage constructively with the development vendor’s findings, communicating issues clearly and specifically enough that remediation was efficient rather than contentious.

The financial services compliance dimension required IV&V review methodology that went beyond functional testing. A payment application’s compliance posture involves data handling, encryption, access control, audit logging, and error handling patterns that require code-level examination rather than interface-level testing. The IV&V team had to evaluate the application against both the bank’s stated requirements and the regulatory standards applicable to a financial institution’s payment processing system.

The quality assurance component of the engagement – automated testing tools combined with manual testing procedures – had to be comprehensive enough to validate functionality, performance, and security across the full range of scenarios the production application would encounter, including edge cases and error conditions that the development team’s own testing may have under-represented. For context on how independent validation integrates with governed application development programs, Integration Governance for MicrosoftPENDING-SCHEDULED covers the change control and governance patterns that make ongoing quality assurance sustainable.

▶ Related Insight — A 60-second perspective from our channel

Selection Rationale (Why They Chose i3solutions)

25+ Years of Development Experience Applied as an Independent Reviewer

The bank needed an IV&V partner whose independence was genuine rather than nominal – a firm with no relationship to the development vendor and no stake in the outcome of the review beyond the quality of its findings. i3solutions had no prior relationship with the development vendor and brought more than 25 years of development and testing experience to the review as an independent perspective rather than a compliance checkbox exercise.

The depth of i3solutions’ development experience was the specific capability that made the IV&V engagement valuable rather than perfunctory. An IV&V review performed by a team that has only ever done testing – and never built systems like the one being reviewed – will identify different and typically less complete sets of issues than a review performed by practitioners who have built payment systems, encountered the failure modes that payment application developers encounter, and know what to look for precisely because they have made and seen similar decisions in their own development work.

The firm’s Enterprise Delivery Assurance model provided the structure that a review engagement of this sensitivity required. Findings were documented with the specificity needed for the development vendor to remediate correctly on the first attempt. Re-testing validated that remediation had addressed the root cause rather than the symptom. The Microsoft consulting services engagement model produced a final sign-off that the bank’s stakeholders could reference as evidence of a rigorous, documented quality process.

The Engagement Approach (Our Plan)

Independent Validation from Code to Production Sign-Off

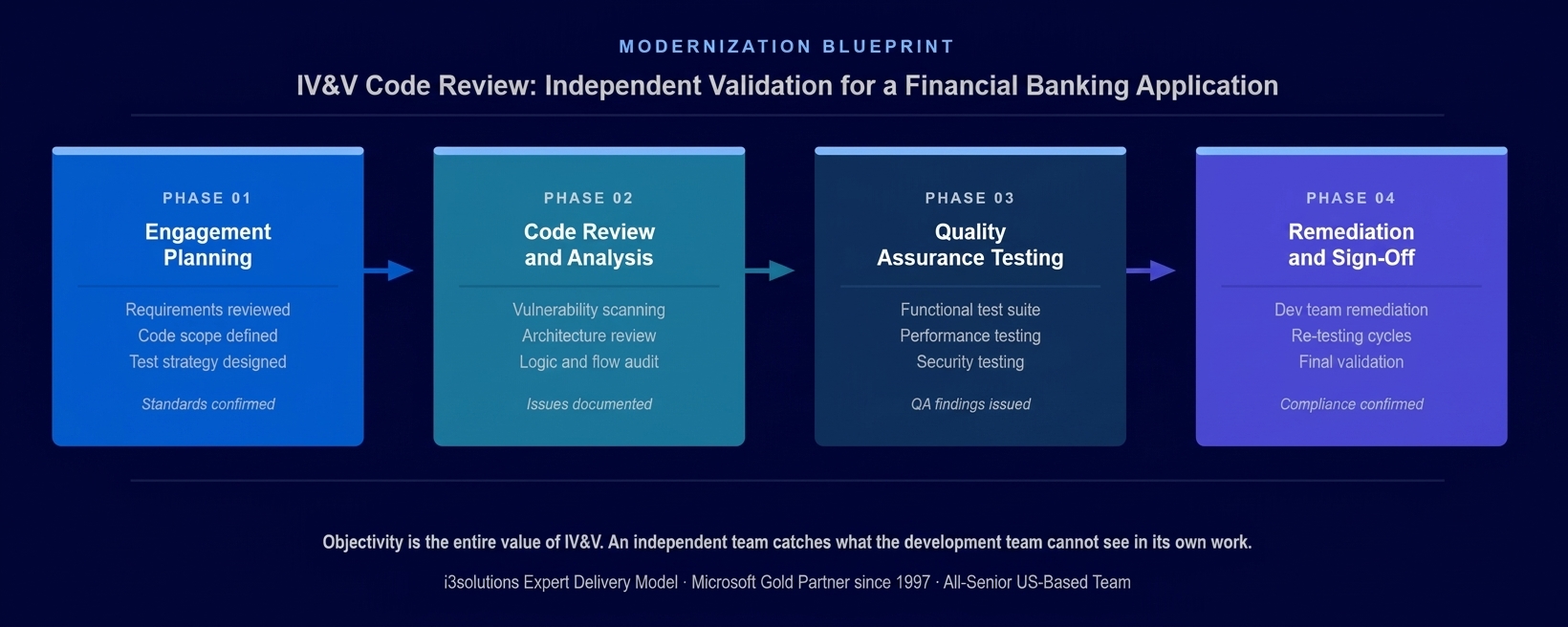

PHASE 01

Engagement Planning and Standards Definition

Reviewing the bank’s requirements documentation, the development vendor’s design specifications, and the applicable compliance standards to establish the review scope and criteria. Defining the IV&V methodology: which automated scanning tools would be applied, which code review areas would receive manual expert examination, which compliance standards would be assessed, and which testing scenarios would exercise the application’s functional, performance, and security requirements. This phase ensured the review had defined success criteria before it began.

PHASE 02

Code Review and Vulnerability Analysis

Performing a comprehensive code review of the Paying Agency Application: automated vulnerability scanning to identify known security issues in the codebase, manual expert examination of the application’s architecture and logic to identify design-level issues that automated tools cannot detect, assessment of the application’s implementation against the bank’s stated requirements to identify gaps or deviations, and evaluation of the data handling, encryption, and access control patterns against financial services compliance standards.

The four-phase IV&V approach. Both automated scanning and manual expert code review were applied – automated tools find known patterns; experienced reviewers find the design-level issues that pattern-matching cannot.

PHASE 03

Quality Assurance Testing

Executing a rigorous quality assurance program combining automated testing tools with manual testing procedures: functional testing validating that the application performed all specified functions correctly across normal and edge-case scenarios, performance testing validating that the application met response time and throughput requirements under the load profiles the production environment would produce, and security testing validating the application’s resistance to the attack patterns applicable to a financial institution’s payment processing system.

PHASE 04

Remediation Validation and Sign-Off

Reviewing the development vendor’s remediation of each identified issue with the specificity needed to confirm that the root cause was addressed rather than the symptom. Re-testing each remediated finding to validate that the fix was correct and did not introduce new issues in adjacent code. Producing the final IV&V sign-off documentation that gave the bank’s stakeholders a clear record of what was reviewed, what was found, how it was remediated, and the basis for the independent conclusion that the application was ready for production deployment.

Execution Evidence

Vulnerabilities Found, Remediated, and Validated Before a Single Transaction

The code review phase surfaced vulnerabilities and compliance gaps that the development team’s own testing had not identified. This was not a reflection of deficient development practice – it was a demonstration of exactly why IV&V exists. The same expertise and familiarity with the codebase that made the development team effective at building the application made them less effective at seeing the specific issues that an independent reviewer with fresh eyes and a different analytical framework would identify immediately.

Each finding was documented with the specificity needed for the development vendor to understand exactly what was wrong, why it was a problem, and what the correct remediation approach was. Ambiguous findings that leave developers guessing at root cause produce inefficient remediation cycles. Specific, well-documented findings produce direct remediation on the first attempt. This specificity – itself a function of the IV&V team’s own development depth – reduced the number of re-testing cycles required and kept the engagement within the project timeline.

The quality assurance testing program was designed to exercise the application across the full range of scenarios the production environment would produce – not just the happy-path scenarios that development teams typically optimize. Edge cases, error conditions, boundary inputs, and concurrent-user scenarios all received specific testing attention. Performance testing confirmed that the application would meet response time requirements under the load conditions of a production banking environment, not just the lower-volume conditions of a development environment.

The engagement’s honest challenge was the timeline pressure. The bank had a target deployment date that the development vendor was working toward, and the IV&V engagement needed to complete its review and remediation validation within that timeline. Managing the pace of findings documentation, vendor remediation, and IV&V re-testing to fit within the project schedule required close coordination between i3solutions, the bank, and the development vendor. This coordination was ultimately productive – the structured IV&V process gave all parties clear milestones and prevented the ambiguity-driven delays that unstructured review engagements often produce.

Technical Transformation

From Unvalidated Application to Independently Certified Production System

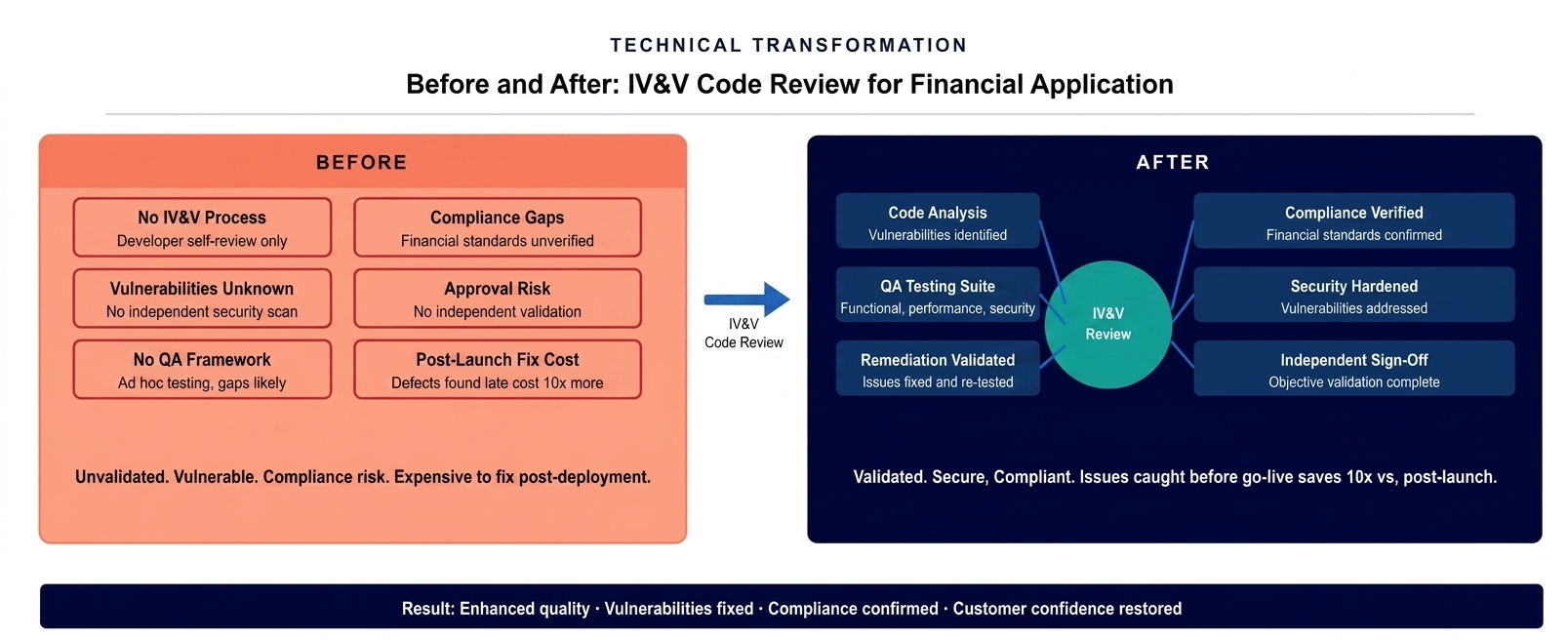

Before the IV&V engagement, the Paying Agency Application was a system in development that had been reviewed and tested only by the team that built it. The quality of the application was a function of the development team’s expertise and diligence – both of which were real, but neither of which could provide the objective validation that a critical financial institution application requires before handling live transactions.

After the IV&V engagement, the application was a system that had been independently examined at the code level, tested across functional, performance, and security dimensions by a team with no investment in the outcome, and signed off with documentation that gave the bank’s stakeholders and regulators a clear basis for confidence that the application had been rigorously validated before deployment.

The validation state before and after the IV&V engagement. An unvalidated development vendor’s application became an independently reviewed, vulnerability-remediated, compliance-confirmed system before the first live transaction.

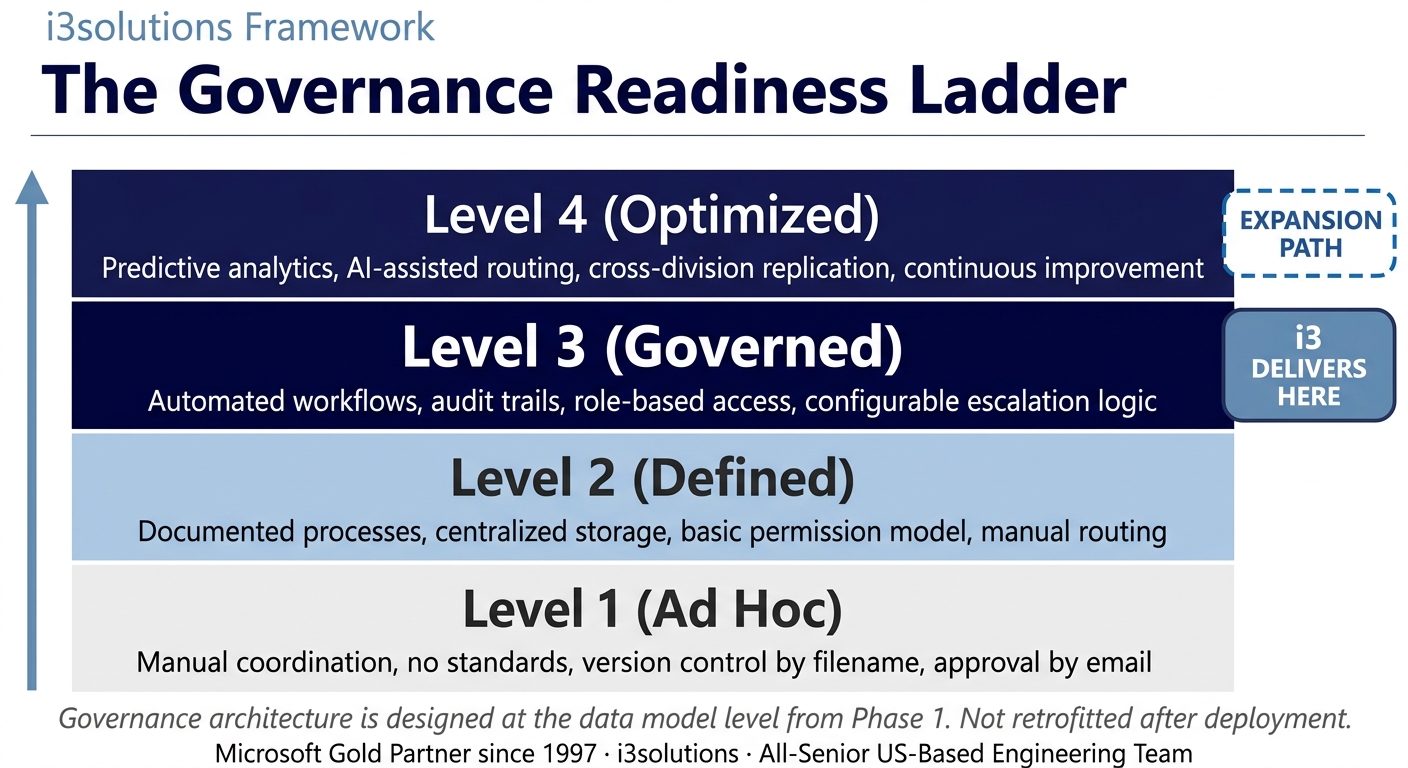

The Governance Readiness Ladder applied to this engagement showed the application development process at Level 1 (Ad Hoc): third-party development with no independent validation, no external compliance review, and no structured quality process beyond the vendor’s own QA. The IV&V engagement advanced the process to Level 3 (Governed): structured independent review with documented findings, compliance validation against applicable standards, performance-validated under production conditions, and a signed-off record of the validation process that the bank could produce in any examination or audit context.

The Governance Readiness Ladder applied to this engagement. The IV&V process delivered Level 3 validation governance for the payment application. The structured approach supports Level 4 as ongoing monitoring and continuous validation programs mature.

▶ Related Insight — A 60-second perspective from our channel

Measurable Outcomes

Vulnerabilities Remediated, Quality Enhanced, Compliance Confirmed, Costs Avoided

| Metric | Before IV&V | After IV&V | Outcome |

|---|

| Application security posture | Unknown – not independently assessed; development team’s own review only | Independently validated; all identified vulnerabilities addressed before production | Security exposure eliminated before go-live |

| Code quality | Vendor-assessed only; objectivity gap inherent in self-review | Independent code review surfaced issues invisible to development team | Application quality independently confirmed |

| Compliance verification | Assumed but not independently verified against financial industry standards | Verified against applicable standards with documented evidence | Compliance independently confirmed |

| Security vulnerabilities | Unknown – not detectable from the inside of the development team | Identified, documented, remediated, and re-tested before deployment | Vulnerabilities remediated before first transaction |

| Cost of defect remediation | Pre-IV&V: relatively low (development vendor engaged, codebase active) | Post-go-live (avoided): 10-100x higher per industry research | Post-launch fix costs avoided BENCHMARK-ESTIMATE |

| Customer satisfaction and confidence | Dependent on unvalidated application performing correctly in production | Application independently validated before customer-facing deployment | Customer confidence grounded in objective validation |

| Regulatory examination posture | No documentation of independent validation for examiner review | Complete IV&V documentation demonstrating rigorous pre-deployment review | Examination-ready documentation produced |

[PENDING-CLIENT-QUOTE: insert 1-3 sentence outcome-focused quote in the client’s own language from a role matching the reader’s role.]

[Name or Role], [Organization type]

The primary value of the IV&V engagement was not in any single finding – it was in the structural certainty it provided. The bank could deploy the Paying Agency Application knowing that an experienced, independent team had examined the code, tested the functionality, assessed the security posture, and validated compliance with applicable standards. That certainty had direct value to the bank’s risk management, its regulatory relationships, and its customer-facing confidence in the system it was deploying on their behalf.

Industry research on defect remediation costs indicates that issues identified and fixed during development cost between 10 and 100 times less than the same issues identified in production. BENCHMARK-ESTIMATE For a payment application handling financial transactions and customer data, the category of post-launch discovery that IV&V prevents is not just more expensive to fix technically – it is more expensive organizationally, reputationally, and regulatorily than any pre-deployment investment in independent validation.

Is a payment or customer-data application approaching deployment without independent validation?

A Risk and Roadmap Assessment maps the IV&V scope, methodology, and timeline appropriate for your specific application’s function, complexity, and applicable compliance standards – before the deadline pressure of an imminent deployment makes thorough validation harder to complete well.

Schedule the Assessment

Credibility Anchors

The Value of Objectivity in a Compliance-Driven Industry

In financial services, objectivity and standards adherence are not abstract values – they are operational requirements. A bank that allows a critical payment application to go live without independent validation is not simply taking a quality risk. It is operating outside the standard of care that its regulators, its auditors, and its customers expect. The IV&V engagement delivered objective validation as a defined, documentable process rather than as a professional opinion – which is precisely the form that financial institution governance requires.

A bank technology leader described the IV&V outcome simply: you spend years building customer trust in your systems. The IV&V engagement was insurance for that trust. Finding out that a vulnerability existed after a customer’s account was affected would have been a completely different situation than finding it during code review and fixing it before anyone was at risk.

The documentation produced by the IV&V engagement served multiple purposes beyond the immediate project. The findings log, remediation record, and final sign-off created a reference document that the bank’s technology governance function could use as the baseline for the application’s ongoing maintenance and change management program. The testing methodology, compliance assessment approach, and code review standards documented in the engagement became templates that the bank could apply to future development projects as its IV&V practice matured.

i3solutions has completed more than 600 Microsoft implementations and technology engagements as a Microsoft Gold Partner since 1997. The combination of 25-plus years of development experience and an independent reviewer’s objectivity is what makes IV&V consulting valuable: the team reviewing the code has built systems like it and knows what to look for, but has no investment in the outcome of what it finds.

Frequently Asked Questions

IV&V Consulting Services for Financial Institution Applications

What is IV&V consulting services for financial applications?

IV&V consulting services for financial applications involve engaging an independent firm to objectively verify that an application being developed by a third-party vendor meets the client’s requirements and industry compliance standards. Independent Verification and Validation provides an objective layer of validation that identifies vulnerabilities, compliance gaps, and quality issues that the development team may be unable to recognize in its own work. In financial services environments where regulatory compliance and data security are baseline requirements, IV&V is a risk management investment rather than a quality preference.

Why do financial institutions need independent code reviews?

Financial institutions need independent code reviews because the development team responsible for building an application cannot objectively validate its own work. Cognitive bias, investment in existing design decisions, and familiarity with the codebase all reduce the team’s ability to identify vulnerabilities and compliance gaps that an independent reviewer with no prior exposure to the code will catch immediately. In regulated financial environments, this independence is often a compliance requirement rather than simply a best practice.

What does an IV&V code review examine?

An IV&V code review examines the application’s code for security vulnerabilities, logic errors, and compliance with the client’s requirements; the application’s architecture for design patterns that create risk or limit maintainability; the completeness and accuracy of the application’s implementation of specified requirements; and the quality and coverage of the development team’s own testing. The IV&V team then documents findings with specific remediation recommendations and validates that remediation has been correctly implemented before sign-off.

How does IV&V differ from regular QA testing?

IV&V differs from regular QA testing in its independence and scope. Regular QA testing is performed by the development team or its designated QA function, which shares the organizational context, design assumptions, and codebase familiarity that can make certain classes of issues invisible. IV&V is performed by a completely independent firm with no prior relationship to the code, which examines not just whether the application works but whether it was built correctly, meets the client’s actual requirements, and complies with applicable industry standards. IV&V also typically includes code review at the source level, not just black-box functional testing.

What compliance standards apply to financial institution applications?

Financial institution applications are subject to compliance standards including PCI DSS for payment card data handling, SOX for financial reporting systems, GLBA for customer financial data protection, and applicable federal and state banking regulations. The specific standards applicable to a given application depend on its function, the data it processes, and the regulatory category of the institution. IV&V reviews for financial applications assess compliance against the standards applicable to the specific application type rather than applying a generic financial services checklist.

How does IV&V reduce the cost of fixing defects?

IV&V reduces the cost of fixing defects by identifying issues before production deployment, when the cost to remediate is an order of magnitude lower than finding the same issue after go-live. Industry research consistently documents that defects found and fixed during development cost between 10 and 100 times less to address than defects discovered in production, where remediation requires emergency development cycles, potential regulatory notification, customer communication, and the reputational cost of a visible failure.

What should financial institutions look for in an IV&V consulting partner?

Financial institutions evaluating IV&V consulting partners should assess the partner’s independence from the development team being reviewed, their experience with financial industry compliance standards, the depth of their code review methodology including both automated scanning and manual expert analysis, and their ability to communicate findings in terms that are actionable for the development team and understandable to business stakeholders. An all-senior review team reduces the risk of findings being missed because a junior reviewer lacked the experience to recognize a specific class of vulnerability.

How long does an IV&V code review take for a financial application?

An IV&V code review for a financial application typically spans several weeks from initial engagement through final sign-off, with timeline driven by the scope and complexity of the application, the number of integrations and data flows requiring review, the volume of remediation required, and the re-testing cycles needed to validate that remediation was correctly implemented. Organizations that engage IV&V reviewers early in the development lifecycle, rather than immediately before planned deployment, allow more time for thorough review and remediation without compressing the project timeline.

Conclusion

Independent Validation Before the First Transaction

A community bank engaged i3solutions to provide IV&V consulting services for a Paying Agency Application being developed by a third-party vendor, deploying more than 25 years of development experience as an independent reviewer to identify vulnerabilities, validate compliance with financial industry standards, test functionality and security across the full range of production scenarios, and certify the application’s readiness for deployment before it handled a single live transaction. The engagement produced the objective documentation that the bank’s stakeholders and regulators expected and the remediated codebase that customers deserved.

For financial institutions deploying third-party developed applications that handle payment processing, customer data, or regulated functions, IV&V consulting services and custom application development offer a documented path from vendor delivery to independently validated, compliance-confirmed production deployment – with the findings documentation to support every subsequent audit and examination.

Back to Case Study Library

60 enterprise Microsoft implementations documented

Related Insights

From the i3solutions YouTube Channel

Short-form perspectives on the delivery and technology challenges in this case study.

Who This Engagement Serves

This engagement is relevant if

- Financial institutions seeking to replace manual spreadsheet verification with automated, independent code validation for complex risk models.

- Banking organizations requiring immutable audit trails and regulatory compliance documentation for their internal financial logic and calculations.

- Lenders needing to eliminate operational risk from key person dependencies in critical, bespoke financial analysis spreadsheets.

Less relevant if

- Smaller banks using standard, off-the-shelf financial software without any custom code or complex internal logic development.

- Organizations relying entirely on SaaS platforms where code review is managed externally by the software vendor.

Ready to give your board and regulators the independent validation they expect?

The 15-Business-Day Microsoft Assessment scopes your IV&V engagement: the review methodology appropriate for your application’s function and compliance requirements, the testing program that exercises production-representative scenarios, and the documentation standard that satisfies both your internal governance and your external examination obligations. Independent. Senior. Documented.

Microsoft Gold Partner since 1997. 600+ implementations. All senior. All US-based.

Schedule the Assessment